The 29th edition of the Knight Frank-FICCI-NAREDCO Real Estate Sentiment Index Q2 2021 (April – June 2021) Survey was released recently. While the survey sounded optimistic about the future outlook, it conceded that the current real estate sentiment has been hit but less severely that it was in the same period last year.

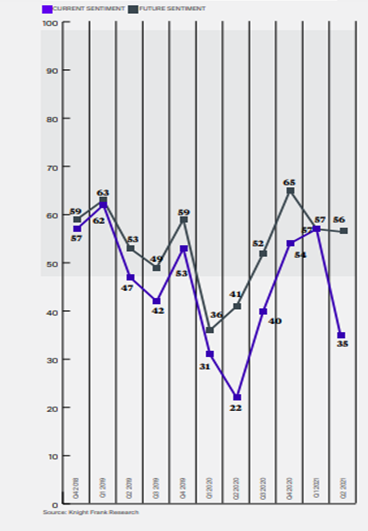

The real estate current sentiment score dropped to 35 in Q2 from 57 in Q1, the lowest in the last 12 months. It was 22 in Q2 2020.

“(It) is indicative of a more resilient market compared to the last time,” the report said.

A score of 50 represents a neutral view or status quo; a score above 50 demonstrates a positive sentiment, and a score below 50 indicates negative sentiment.

“Though the second wave of the pandemic was more damaging to health and life than the first one, the negative impact it had on market sentiments was comparatively less”, the report said.

The report said that the Future sentiment score inched down marginally from 57 in Q1 2021 to 56 in Q2 2021, indicating the continuity in a positive outlook of market stakeholders.

The Future Sentiment score takes into account the stakeholder outlook of the real estate sector for the coming six months.

“As lockdowns are being gradually lifted, mobility restrictions are being relaxed phase-wise, offices are opening up and the country is transitioning into the post-second wave phase. These developments have helped keep the stakeholder outlook positive for the next six months,” the report said.

The future sentiment score in North India stood at 55 in Q2 2021 a marginal drop from 56 in Q1, 58 in Q4 2020, 55 in Q3 2020, and 38 in Q2 2020.

The report said that the developer outlook has improved but the non-developer outlook has weakened. Even as both remained in the optimistic zone, the developer outlook has increased from 54 in Q1 2021 to 56 in Q2 2021 while the non-developer outlook has weakened from 64 in Q1 2021 to 56 in Q2 2021.

The Real Estate Sentiment Index is based on a quarterly survey of key supply-side stakeholders which include developers and non-developers.

As for residential outlook, the survey pointed out that 64% of the respondents in Q2 2021, the same as in Q1 2021, expect residential sales to increase in the next six months. The share of respondents expecting a decline in new project launches increased from 9% in Q1 2021 to 22% in Q2 2021.

With regard to residential prices, the report said that 47% of the Q2 2021 survey respondents – up from 43% in Q1 2021 – expect prices to remain stable in the next six months, while 45% of Q2 2021 survey respondents believe that prices will increase.

As for offices, they said that 40% of the Q2 2021 survey respondents – up from 34% in Q1 2021 – expect office space leasing to increase in the next six months. 69% of the Q2 2021 survey respondents – marginally down from 70% in Q1 2021 are of the opinion that the new office supply will either increase or remain the same over the next six months. 21% of the Q2 2021 survey respondents – up from 15% in Q1 2021 – expect office rents to increase in the next six months, while 40% expect rents to remain stable

On the economic front, 84% of the Q2 2021 survey respondents – down marginally from 85% of Q1 2021 – still expect the economic scenario to improve or remain at the present levels for the next six months.